What is garment costing?

Garment costing is the process of assigning a monetary value to every resource used to make a garment, including materials, trims, labour, conversion charges, and overhead, to determine the cost per unit that drives pricing and margin.

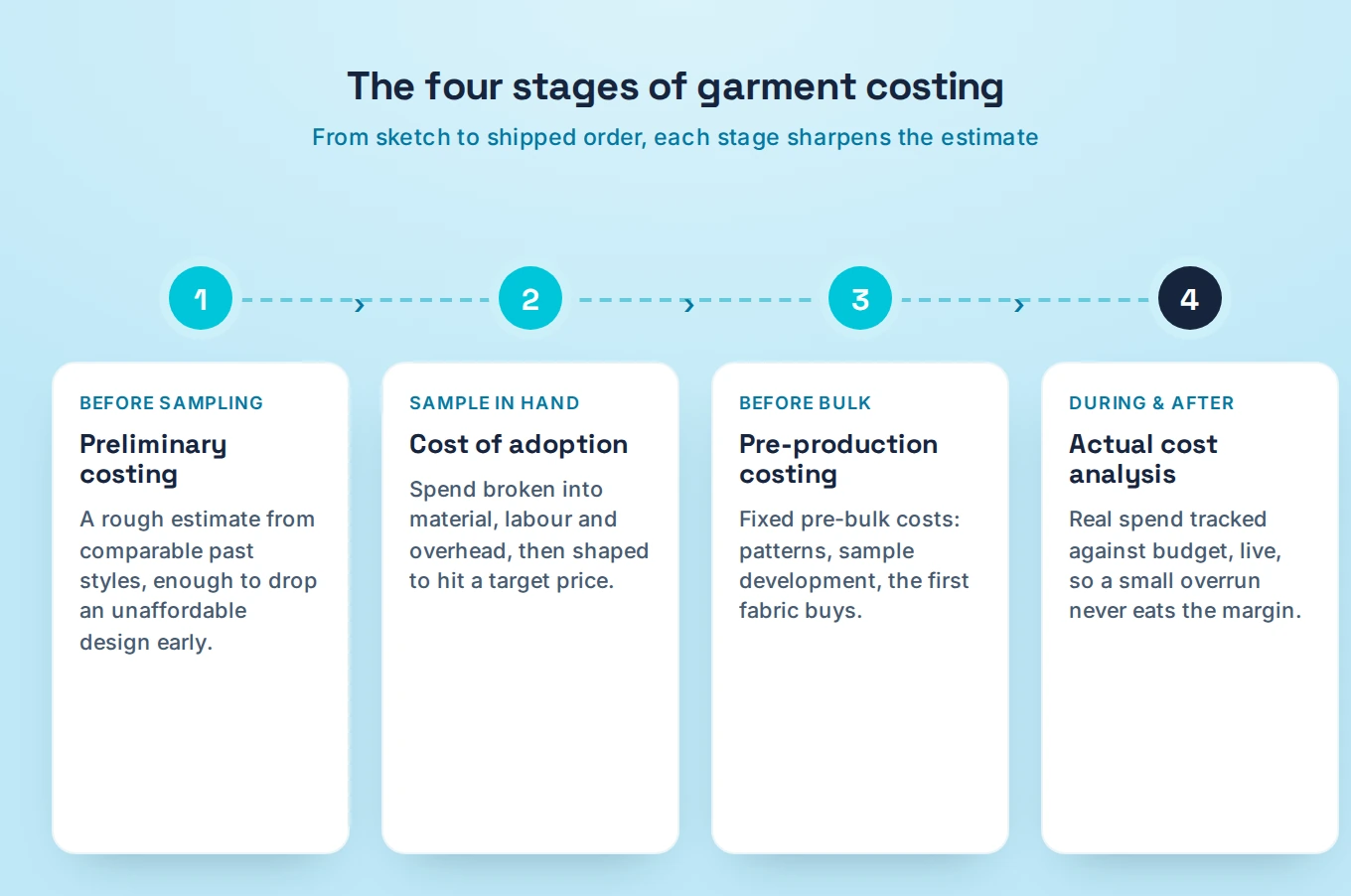

What are the four stages of garment costing?

The four stages are preliminary (pre) costing, cost of adoption, pre-production costing, and actual cost analysis. Each tightens the estimate as the design moves from concept to finished product.

What percentage of a garment’s cost is fabric?

Fabric is the single largest component, typically 60 to 70% of the cost of a basic style garment. The figure rises for premium fibres and complex designs.

What is the difference between absorption costing and variable costing?

Absorption costing allocates both fixed and variable manufacturing overhead to each unit and is required under GAAP for external reporting. Variable costing includes only variable costs and is used internally for short-term decisions.

What is CMT in garment costing?

CMT stands for cut, make, trim, the cost of making a garment. It is calculated as cost per hour multiplied by the hours to make the style, divided by units produced, and includes the contractor’s profit.

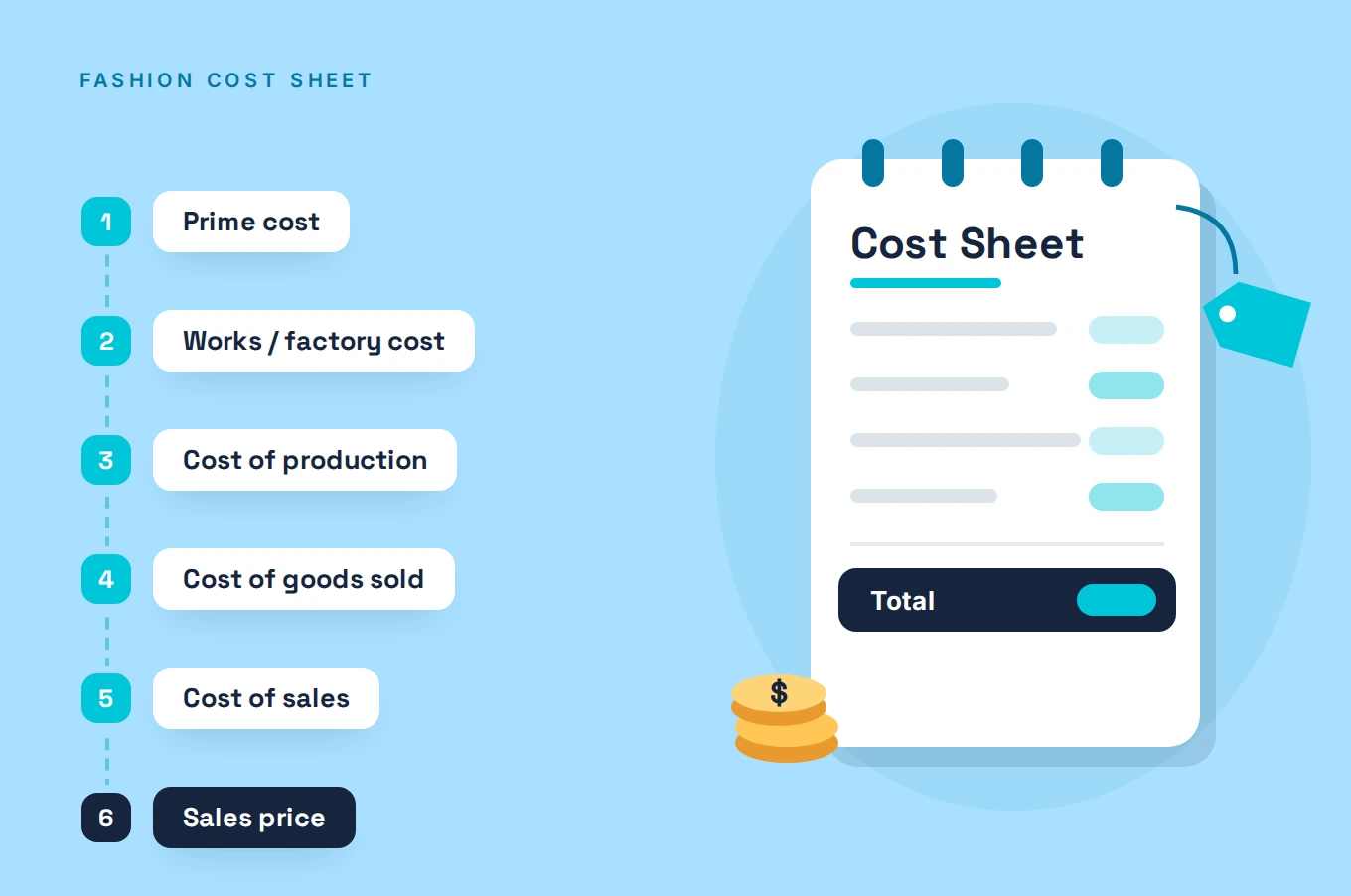

What goes into a fashion cost sheet?

A cost sheet builds up from direct materials, labour, and expenses (prime cost), then adds factory overhead (works cost), administrative overhead (cost of production), selling overhead, and profit to reach the sales price.

How does ERP software reduce garment manufacturing costs?

ERP reduces costs by optimising inventory, automating manual tasks, improving data access, maximising material utilisation, and tracking sampling, all within a single system where estimated and actual costs stay reconciled.